Reverse convertible securities Contents Description Maturity options Liquidity Ratings Taxes Investor benefits Risk to consider See also References Navigation menu"Reverse Converts: A Nest-Egg Slasher?"the original"The reverse convertible bond sparks a lively debate"Manufacturing and Managing Customer-Driven Derivativese

InvestmentSecurities (finance)

stocksecuritycoupon ratepar valueequitymaturitystructured productsoffering circularbuy and holdliquidity30/360actual/365Bloomberg L.P.U.S. Securities and Exchange Commissionunsecured debtput optioncapital gain

A reverse convertible security or convertible security is a short-term note linked to an underlying stock. The security offers a steady stream of income due to the payment of a high coupon rate. In addition, at maturity the owner will receive either 100% of the par value or, if the stock value falls, a predetermined number of shares of the underlying stock.[1] In the context of structured product, a reverse convertible can be linked to an equity index or a basket of indices. In such case, the capital repayment at maturity is cash settled, either 100% of principal, or less if the underlying index falls conditional on barrier is hit in the case of barrier reverse convertibles.

Contents

1 Description

1.1 Features

1.2 Reference shares

1.3 How do reverse convertibles work?

2 Maturity options

2.1 Delivery at maturity

2.2 Physical delivery

2.3 Scenario 1 – cash delivery

2.4 Scenario 2 – cash delivery

2.5 Scenario 3 – physical delivery

3 Liquidity

3.1 Trading

4 Ratings

5 Taxes

6 Investor benefits

7 Risk to consider

8 See also

9 References

Description

Features

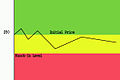

These are short-term coupon bearing notes, which are designed to provide an enhanced yield while maintaining certain equity-like risks. Their investment value is derived from the underlying equity exposure, paid in the form of fixed coupons. Owners receive full principal back at maturity if the Knock-in Level is not breached (which is typically 70-80% of the initial reference price). If the underlying stock falls in value, the investor will receive shares of stock which will be worth less than his original investment. The underlying stock, index or basket of equities is defined as Reference Shares. In most cases, Reverse convertibles are linked to a single stock.

You may also find inverse reverse convertibles, which are the opposite of a reverse convertible. The owner benefits as long the underlying stock does not go above a predetermined barrier. If the underlying stock breaches the barrier, the owner will receive the principal minus the percentage of the movement against him.

These are both types of structured products, which are sophisticated instruments and carry a significant risk of loss of capital.[2]

In a low interest rate and high market volatility environment, reverse convertibles are popular as they provide much enhanced yield for the investors. By receiving enhanced coupons, investors take on the risk of losing part of the capital. Prior to the turn of the millennium (2000), reverse convertibles mostly consisted of investors shorting standard at-the-money (ATM) put options. Investors would lose capital if at maturity the underlying fell below the initial level. To increase the protection for investors, barrier reverse convertibles were introduced whereby investors were instead shorting ATM down-and-in put options. The additional barrier event increased the protection for the investors, as the put option would not come into effect unless the (down) barrier was hit. The barrier protection feature triggered much increased reverse convertible issuances in UK in the early 2000s as well as in the European retail markets. By the early 2010s, the (barrier) reverse convertibles were also among the most popular structured products in US.

While the barrier protection feature was beneficial for investors, for the issuers, managing and hedging relatively long-dated (e.g. 3~5 years) equity barrier risks were a serious challenge. The hedging parameters (Greeks) near the barrier could be unstable, and they could suddenly change which would lead to a massive increase in trading volumes in the process of hedging. In contrast to FX underlyings, equity underlyings for the reverse convertibles tend to have much less liquidity. The problems would become more severe as and when the products were introduced to the mass retail market. To solve these practical problems during the product design process, various technologies [3] were adopted in the barrier reverse convertible pricing models to deal with barrier concentration risks. Reverse convertibles nowadays account for a large portion the structured products issued for retail and private investors. The issuances of other breeds of reverse convertibles, such as those combining a callable payoff, or a knockout clause, have also increased substantially [4] with the ever changing market conditions.

- Underlying stocks or basket of equities may include names such as:

- Dell

- Wal-Mart

- Exxon Mobil

- Cisco

- Best Buy

- Corning

- Broad market indices may include names such as:

- RSI Diversified Index

- S&P-500 Index

- EURO STOXX-50 Index

- FTSE-100 Index

- NIKKEI-225

- Nasdaq-100 Index

How do reverse convertibles work?

They are short-term investments, typically with a one-year maturity. At maturity, the owner receives either 100% of their original investment or a predetermined number of shares of the underlying stock, in addition to the stated coupon payment. The owner's earning potential is limited to the security’s stated coupon, because he receives coupon payments regardless of the performance of the underlying reference shares. Risk potential is the same as for the underlying security, less the coupon payment.

Coupon payments are the obligation of the issuer and are paid on a monthly or quarterly basis. These instruments are sold by prospectus or offering circular, and prices on these notes are updated intra day to reflect the activity of the underlying equity. The rule of thumb is: The higher the coupon payment, the greater likelihood of receiving stock at maturity.

Note: Coupon rate is determined by issuer. Sometimes holders do expect zero coupon bond like reverse convertible bonds.

Maturity options

Delivery at maturity

At maturity, there are two possible outcomes:

Cash Delivery: If the stock closes at or above the initial share price upon valuation date, regardless of whether the stock closed below the knock-in level during the holding period, or if the stock closes below the initial share price, but has never closed below the knock-in level.

Physical Delivery: If the underlying shares closed below the knock-in level at any time during the holding period and does not trade back up above the initial share price on valuation date (four days prior to maturity).

Physical delivery

The initial share price is determined on the trade date. The final valuation of the shares is based on the closing price of the reference shares determined four days prior to maturity. If the investor is delivered physical shares, their value will be less than the initial investment.

Scenario 1 – cash delivery

| Reference share closing price is above the initial share price of the note on valuation date (four days prior to maturity), regardless of whether the stock closed below the knock-in level. Investor receives "Cash Delivery Amount" (Par), at maturity.[5] |

Scenario 2 – cash delivery

| Reference share closing price is below the initial share price of the note on valuation date (four days prior to maturity), but never closed below the knock-in level. Investor receives "Cash Delivery Amount" (Par) at maturity.[5] |

Scenario 3 – physical delivery

| Reference share closing price is below the initial price of the note at valuation date (four days prior to maturity), and has closed below the downside knock-in level during the holding period. Investors receive "Physical Delivery Amount", or shares of stock, at maturity. Predetermined number of shares delivered to the investor if closing price of reference shares below initial price.[5] Physical Delivery Amount = |

Liquidity

These are generally created as a buy and hold investment, but issuers typically provide liquidity in the secondary market. The secondary market price may not immediately reflect changes in the underlying security. Liquidations prior to maturity may be less than the initial principal amount invested.

Trading

They trade flat and accrue on a 30/360 or actual/365 basis. End of day pricing is posted on Bloomberg L.P. and/or the internet. Pricing fluctuates intraday. Reverse Convertibles are registered with the U.S. Securities and Exchange Commission (SEC).

Ratings

These are an unsecured debt obligation of the issuer, not the reference company, thus they carry the rating of the issuer. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations.

Taxes

For tax purposes Reverse convertible notes are considered to have two components: a debt portion and a put option. At maturity, the option component is taxed as a short-term capital gain if the investor receives the cash settlement. In the case of physical delivery, the option component will reduce the tax basis of the Reference Shares delivered to their accounts.

Investor benefits

These securities can offer enhanced yield and current income at the cost of higher risk. They also carry downside protection, typically up to 10-30% on most Reverse Convertible offerings. The bid-ask spread is typically 1%.

Risk to consider

- The price of the reference shares may decline during the term of the note, which will affect the investor negatively, while the investor does not have the same price appreciation potential as the reference shares, because at maturity the most the investor will receive is his original principal amount.

- Investors selling notes prior to maturity may receive a market price which may be higher or lower than par value, not necessarily reflecting any increase or decrease in the market price of the underlying equity.

- Reverse convertibles do not guarantee return of principal at maturity.

- The market price of the Reverse convertibles may be influenced by unpredictable market factors.

- If the underlying security issues a previously unannounced special dividend, and the security were to trade ex-dividend prior to maturity of the reverse convertible, it is possible that an investor in the structure may suffer a capital loss, as they are not eligible to receive the special dividend.

See also

- Convertible bond

- Convertible security

- Exchangeable bond

- Structured product

References

^ Light, Larry (June 16, 2009). "Reverse Converts: A Nest-Egg Slasher?". online.wsj.com. Archived from the original on June 18, 2009..mw-parser-output cite.citationfont-style:inherit.mw-parser-output .citation qquotes:"""""""'""'".mw-parser-output .citation .cs1-lock-free abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/6/65/Lock-green.svg/9px-Lock-green.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .citation .cs1-lock-limited a,.mw-parser-output .citation .cs1-lock-registration abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/d/d6/Lock-gray-alt-2.svg/9px-Lock-gray-alt-2.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .citation .cs1-lock-subscription abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/a/aa/Lock-red-alt-2.svg/9px-Lock-red-alt-2.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .cs1-subscription,.mw-parser-output .cs1-registrationcolor:#555.mw-parser-output .cs1-subscription span,.mw-parser-output .cs1-registration spanborder-bottom:1px dotted;cursor:help.mw-parser-output .cs1-ws-icon abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/4/4c/Wikisource-logo.svg/12px-Wikisource-logo.svg.png")no-repeat;background-position:right .1em center.mw-parser-output code.cs1-codecolor:inherit;background:inherit;border:inherit;padding:inherit.mw-parser-output .cs1-hidden-errordisplay:none;font-size:100%.mw-parser-output .cs1-visible-errorfont-size:100%.mw-parser-output .cs1-maintdisplay:none;color:#33aa33;margin-left:0.3em.mw-parser-output .cs1-subscription,.mw-parser-output .cs1-registration,.mw-parser-output .cs1-formatfont-size:95%.mw-parser-output .cs1-kern-left,.mw-parser-output .cs1-kern-wl-leftpadding-left:0.2em.mw-parser-output .cs1-kern-right,.mw-parser-output .cs1-kern-wl-rightpadding-right:0.2em

^ Staff, A. O. L. "The reverse convertible bond sparks a lively debate". AOL.com.

^ Qu, Dong, (2001). "Managing Barrier Risks Using Exponential Soft Barriers". Derivatives Week, (15 January)

^ Qu, Dong (2016). Manufacturing and Managing Customer-Driven Derivatives. Wiley.

ISBN 978-1-118-63262-8.

^ abc https://www.fisbonds.com/fisdocuments/managedContent/AAMSecurities/RCN%2520Whitepaper%2520FINAL%2520%28719%29%2520060107.pdf